The payback period is a simple capital budgeting method used to determine the length of time required to recover the initial investment of a project or asset. It’s a popular technique due to its ease of calculation and understanding, providing a quick assessment of a project’s liquidity.

Payback Formula

The basic formula for calculating the payback period is:

Payback Period = Initial Investment / Annual Cash Inflow

This formula is applicable when the annual cash inflows are consistent throughout the project’s life. For example, if a project requires an initial investment of $100,000 and generates annual cash inflows of $25,000, the payback period would be $100,000 / $25,000 = 4 years.

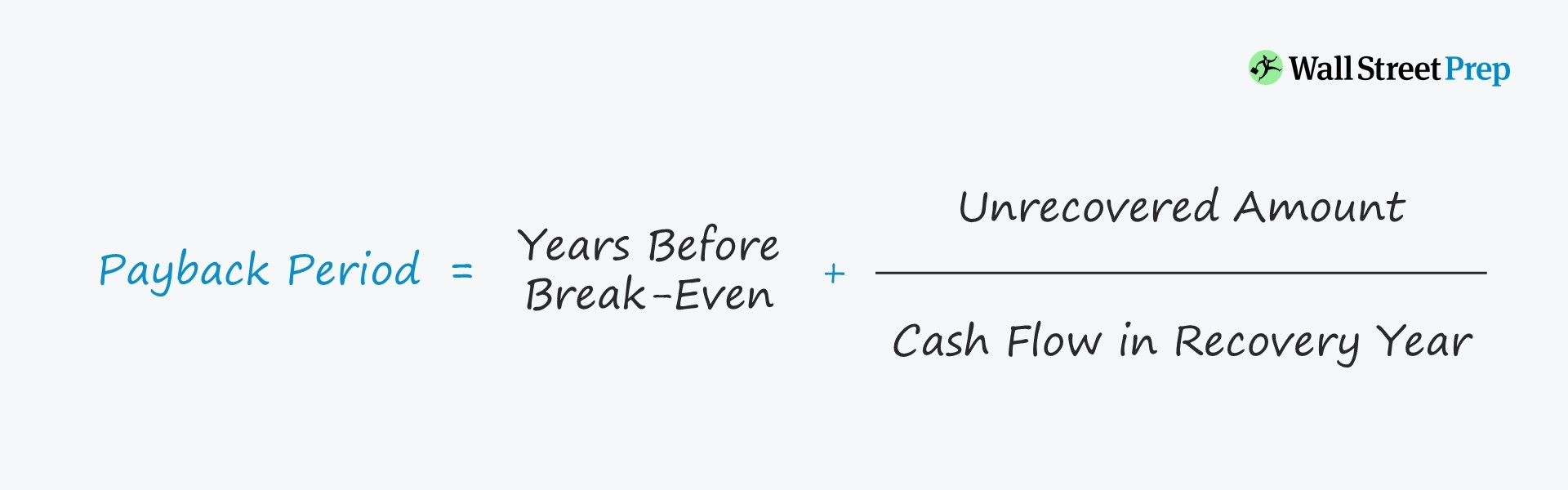

However, many projects don’t have uniform cash inflows. In such cases, the payback period is calculated by accumulating the cash inflows until the initial investment is recovered. The formula becomes more complex, requiring a step-by-step approach:

- Calculate the cumulative cash inflows for each period (usually years).

- Identify the year in which the cumulative cash inflows exceed the initial investment.

- Calculate the fraction of the final year required to recover the remaining investment: (Unrecovered Investment at the Beginning of the Year) / (Cash Inflow During the Year)

- Add this fraction to the number of full years it took to reach the point where the cumulative cash inflows were less than the initial investment.

For instance, consider a project with an initial investment of $50,000 and the following annual cash inflows: Year 1: $10,000, Year 2: $15,000, Year 3: $20,000, Year 4: $10,000.

- Year 1: Cumulative inflow = $10,000 (Unrecovered investment: $40,000)

- Year 2: Cumulative inflow = $25,000 (Unrecovered investment: $25,000)

- Year 3: Cumulative inflow = $45,000 (Unrecovered investment: $5,000)

The payback occurs between Year 2 and Year 3. The fraction of Year 3 needed is $5,000 / $20,000 = 0.25 years. Therefore, the payback period is 2.25 years.

Advantages of Payback Period

- Simplicity: Easy to understand and calculate.

- Liquidity Focus: Highlights projects that quickly recover the initial investment, reducing risk and improving short-term cash flow.

- Useful for Small Businesses: Particularly helpful for companies with limited access to capital.

Disadvantages of Payback Period

- Ignores Time Value of Money: Doesn’t account for the fact that money received today is worth more than money received in the future.

- Ignores Cash Flows Beyond Payback: Doesn’t consider profitability or cash flows occurring after the payback period, potentially leading to rejection of highly profitable long-term projects.

- Arbitrary Cutoff: Selection of the acceptable payback period is often subjective.

In conclusion, the payback period is a useful tool for initial screening and quick assessment of project risk, but it should not be used as the sole criterion for investment decisions. It’s crucial to supplement it with other, more sophisticated capital budgeting techniques, such as Net Present Value (NPV) and Internal Rate of Return (IRR), to get a more complete picture of a project’s profitability and overall value.

1280×854 payback period calculator calculate investment return from www.pinterest.com

1280×854 payback period calculator calculate investment return from www.pinterest.com  1024×526 payback period formula calculator excel template from www.educba.com

1024×526 payback period formula calculator excel template from www.educba.com  1120×167 payback period formula gariavyansh from gariavyansh.blogspot.com

1120×167 payback period formula gariavyansh from gariavyansh.blogspot.com  525×487 payback period calculation formula irsalainrytis from irsalainrytis.blogspot.com

525×487 payback period calculation formula irsalainrytis from irsalainrytis.blogspot.com  1376×268 payback period learn calculate payback period from corporatefinanceinstitute.com

1376×268 payback period learn calculate payback period from corporatefinanceinstitute.com  1280×720 payback period formula tracyhaumie from tracyhaumie.blogspot.com

1280×720 payback period formula tracyhaumie from tracyhaumie.blogspot.com  0 x 0 payback analysis formula lesson studycom from study.com

0 x 0 payback analysis formula lesson studycom from study.com  2020×1007 payback period chart from mungfali.com

2020×1007 payback period chart from mungfali.com  638×479 payback analysis from www.slideshare.net

638×479 payback analysis from www.slideshare.net  940×410 simple payback period elucidate education from www.elucidate.org.au

940×410 simple payback period elucidate education from www.elucidate.org.au  1024×526 payback period definition formula calculate from www.wallstreetmojo.com

1024×526 payback period definition formula calculate from www.wallstreetmojo.com  300×248 payback method formula explanation advantages from www.accountingformanagement.org

300×248 payback method formula explanation advantages from www.accountingformanagement.org  467×304 payback period summary forum manage from www.12manage.com

467×304 payback period summary forum manage from www.12manage.com  625×90 payback period pbp formula calculation method from www.myaccountingcourse.com

625×90 payback period pbp formula calculation method from www.myaccountingcourse.com  620×240 lighting payback period calculator americanwarmomsorg from americanwarmoms.org

620×240 lighting payback period calculator americanwarmomsorg from americanwarmoms.org  320×185 payback period explained formula calculate from www.slideshare.net

320×185 payback period explained formula calculate from www.slideshare.net  800×200 discounted payback period definition formula calculation from www.freshbooks.com

800×200 discounted payback period definition formula calculation from www.freshbooks.com  705×907 solved payback periodthe payback method helps firms cheggcom from www.chegg.com

705×907 solved payback periodthe payback method helps firms cheggcom from www.chegg.com  689×517 payback period business tutoru from www.tutor2u.net

689×517 payback period business tutoru from www.tutor2u.net  1920×600 cuota de admision curva realeza formula calculo payback mezcla canal from mappingmemories.ca

1920×600 cuota de admision curva realeza formula calculo payback mezcla canal from mappingmemories.ca  1869×523 payback period template resume template ideas from resumetemplatesidea.blogspot.com

1869×523 payback period template resume template ideas from resumetemplatesidea.blogspot.com  1280×720 payback period formula from ar.inspiredpencil.com

1280×720 payback period formula from ar.inspiredpencil.com