Generalized Additive Models in Finance

Generalized Additive Models (GAMs) offer a powerful and flexible approach to statistical modeling in finance, bridging the gap between linear models and more complex, often less interpretable, machine learning techniques. In essence, a GAM models a dependent variable as the sum of smooth, potentially nonlinear functions of independent variables. This allows for the capture of complex relationships without sacrificing interpretability, a critical factor in financial applications.

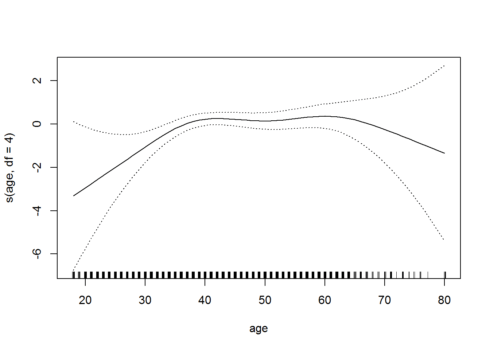

The core idea behind a GAM is the equation: E(Y) = α + f1(X1) + f2(X2) + … + fp(Xp), where Y is the dependent variable, α is the intercept, and fi(Xi) are smooth functions of the independent variables Xi. These smooth functions, typically splines or other nonparametric smoothers, are estimated from the data, allowing the model to adapt to the underlying relationships without imposing strict parametric assumptions.

In finance, GAMs find application in various areas. For instance, credit risk modeling can benefit significantly. Traditional credit scoring models often assume linear relationships between creditworthiness and factors like income, debt, and credit history. GAMs can uncover nonlinear relationships, such as a diminishing impact of income beyond a certain threshold or a more severe penalty for low credit scores than predicted by linear models. This leads to more accurate risk assessments and better loan decisions.

Time series analysis is another fruitful area. GAMs can model trends and seasonality in financial time series data, such as stock prices or interest rates. Unlike traditional ARIMA models, GAMs can handle complex, nonlinear patterns in the data, including regime shifts or time-varying volatility. This allows for improved forecasting and risk management.

Furthermore, GAMs are valuable in option pricing. The Black-Scholes model relies on assumptions that are often violated in practice. GAMs can incorporate factors like volatility smiles or skews, which reflect the market’s perception of risk at different strike prices. By modeling the relationship between option prices and underlying asset characteristics using smooth functions, GAMs can provide more accurate option pricing models.

The interpretability of GAMs is a significant advantage in finance. Each smooth function fi(Xi) can be visualized, allowing analysts to understand the impact of each variable on the dependent variable. This insight is crucial for making informed decisions and justifying model outputs to stakeholders. While machine learning models like neural networks can achieve high accuracy, their “black box” nature can be problematic in regulated environments where transparency is essential.

However, GAMs are not without limitations. They can be computationally intensive, especially with large datasets. Feature selection and model selection (e.g., choosing the appropriate smoothers and regularization parameters) can also be challenging. Nevertheless, the flexibility, interpretability, and predictive power of GAMs make them a valuable tool for financial modeling and analysis.

1025×999 generalized additive models from m-clark.github.io

1025×999 generalized additive models from m-clark.github.io  300×170 overview generalized additive models papers code from paperswithcode.com

300×170 overview generalized additive models papers code from paperswithcode.com  490×350 generalized additive models datascience from datascienceplus.com

490×350 generalized additive models datascience from datascienceplus.com  576×432 introduction generalized additive models from m-clark.github.io

576×432 introduction generalized additive models from m-clark.github.io  640×640 generalized additive models scientific diagram from www.researchgate.net

640×640 generalized additive models scientific diagram from www.researchgate.net  1024×768 generalized additive models powerpoint from www.slideserve.com

1024×768 generalized additive models powerpoint from www.slideserve.com  250×250 university guelph bookstore generalized additive models from bookstore.uoguelph.ca

250×250 university guelph bookstore generalized additive models from bookstore.uoguelph.ca  640×480 generalized additive models ai basics ai from www.aionlinecourse.com

640×480 generalized additive models ai basics ai from www.aionlinecourse.com  850×466 generalized additive models gams threshold generalized additive from www.researchgate.net

850×466 generalized additive models gams threshold generalized additive from www.researchgate.net  850×1100 generalized gloves neural additive models pursuing transparent from deepai.org

850×1100 generalized gloves neural additive models pursuing transparent from deepai.org  850×1100 generalized additive model selection deepai from deepai.org

850×1100 generalized additive model selection deepai from deepai.org  1344×960 generalized additive models foundations applied statistics from jdstorey.org

1344×960 generalized additive models foundations applied statistics from jdstorey.org  1344×960 generalized additive models educational research techniques from educationalresearchtechniques.com

1344×960 generalized additive models educational research techniques from educationalresearchtechniques.com  1600×2428 generalized additive models taylor francis group from www.taylorfrancis.com

1600×2428 generalized additive models taylor francis group from www.taylorfrancis.com  240×320 generalized additive models generalized additive modelspdf pdfpro from pdf4pro.com

240×320 generalized additive models generalized additive modelspdf pdfpro from pdf4pro.com  984×513 generalized additive model examples assumptions from www.wallstreetmojo.com

984×513 generalized additive model examples assumptions from www.wallstreetmojo.com  1024×768 biostatistics lecture generalized additive models powerpoint from www.slideserve.com

1024×768 biostatistics lecture generalized additive models powerpoint from www.slideserve.com  1179×780 generalized additive model delicatessen documentation from deli.readthedocs.io

1179×780 generalized additive model delicatessen documentation from deli.readthedocs.io  5640×3190 creating generalized additive model scratch lazy mathematician from grantlawley.github.io

5640×3190 creating generalized additive model scratch lazy mathematician from grantlawley.github.io  587×587 final generalized additive models characteristics from www.researchgate.net

587×587 final generalized additive models characteristics from www.researchgate.net  640×640 generalized additive models employed show link cu from www.researchgate.net

640×640 generalized additive models employed show link cu from www.researchgate.net  240×320 generalized additive models gams github pages generalized from pdf4pro.com

240×320 generalized additive models gams github pages generalized from pdf4pro.com  672×480 generalized additive models data analysis from geomoer.github.io

672×480 generalized additive models data analysis from geomoer.github.io  850×1276 usage generalized additive models discrete from www.researchgate.net

850×1276 usage generalized additive models discrete from www.researchgate.net